share

share

|

|

Leonard Woo |

|

Chong Su Lyn |

You now have a company and you are thinking of raising funds to expand the business. How would you go about determining the value your company? What are some key considerations for the valuation?

A. VALUATION FRAMEWORK AS A GUIDE

Warren Buffet once said, “Price is what you pay, value is what you get”. In other words, price and value are different. Prices are driven by market sentiments and momentum, which can be disconnected from the intrinsic value of the asset.

There are many examples of how valuations of start-ups can be sky-high even without a history of making profits or with business models that are in their infancy. The question is, therefore, whether the valuation truly reflects the intrinsic value of these start-ups. This reminds us to consider and address fundamental issues that arise when valuing start-ups. For example, can the start-up deliver profitability in the future when historical information does not support this position? Does the start-up really own a competitive advantage that justifies a hockey stick revenue growth rate? Is the start-up’s business model so robust and unique that would allow it to perform above current industry averages? How much will the start-up’s market share and revenues erode if a new entrant creates price wars?

There is no single solution that can be applied to address all these questions. However, if a valuation framework is put in place that provides a structured approach in valuing a start-up, these fundamental elements would at least be properly considered in the valuation process.

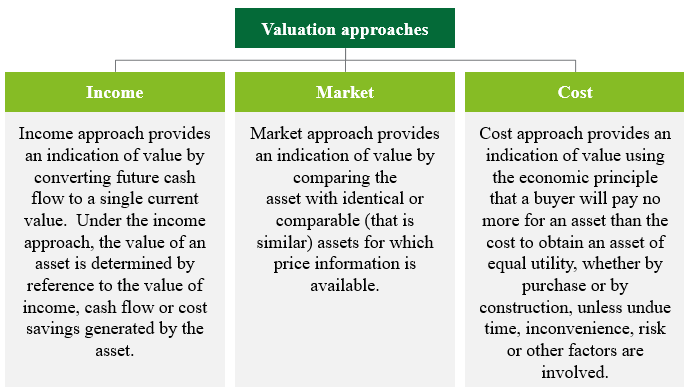

Valuation approaches

The International Valuation Standards defines the principal valuation approaches as follows:[1]

(a) The income approach: discounted cash flow method

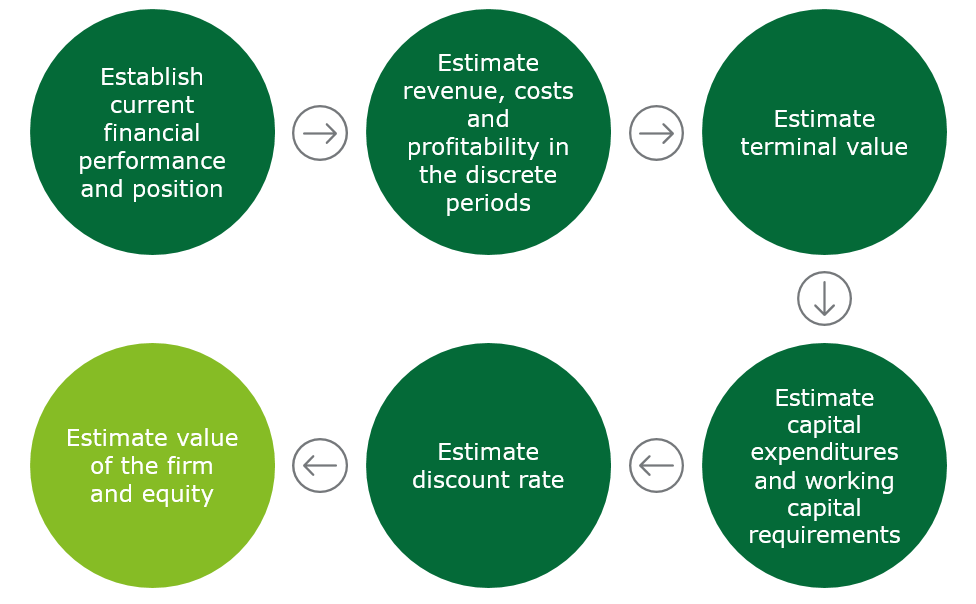

The income approach is applied by discounting future cash flows to present value. This discounted cash flow (“DCF”) method estimates the intrinsic value of the business. It is based on the premise that the value of a business should be equal to the present value of its expected cash flows. The following are the general steps that valuation practitioners and experts such as Professor Aswath Damodaran consider when applying the DCF method:

(i) Establish current financial performance and position

When valuing a firm, information on earnings and assets are used as inputs in the valuation process. Financial statements are often depended on to assess a firm’s current financial performance and position.

However, it should be kept in mind that the stability of revenues, earnings and cash flows generated by a firm would change over its life cycle. A start-up is more likely to generate revenues, earnings and cash flows that are more volatile compared to a mature firm. Hence, information from the last financial year may not be the most updated information on the start-up’s financial potential. Using the latest available financial information such as from the twelve months prior to valuation date will provide a better estimate of value compared to using information from the last financial year. [2]

(ii) Estimate revenue, costs and profitability in the discrete periods

Frequently, one of the major issues that arises in valuing start-ups is the difficulty in assessing whether the estimated cash flows are sustainable for both the discrete and terminal periods. To make the assessment, the historical revenue growth rates of the start-up could be considered first. However, firstly, by their very definition, start-ups are young firms with limited history. This means that they have little historical financial information and projected cash flows must be built from scratch. Secondly, start-ups may also be making losses or have negative cash flows, making it even tougher to project profitability margins. Further, the target markets of new ventures are likely to be highly dynamic in terms of growth, size of customer base and disruption by other competitors. This makes it difficult to assess whether projections are achievable.

In order to address some of the issues raised, market information may serve as guidance. Firstly, a start-up is more likely to be able to maintain high growth rates if the markets that they serve are also growing at high growth rates.[3] Secondly, revenue growth rates, costs and profitability margins of publicly-traded companies within the same market as the start-up can be used as benchmarks.

While market information may be valuable, it may also be difficult to identify the market that the start-up is serving. If the start-up’s service offering is truly innovative, it may not be possible to identify a market at first glance. In this case, one should consider the market or industry that the start-up is disrupting. For example, while ride-hailing start-ups are tech companies, they are essentially disrupting the local taxi service business. As such, when assessing whether revenue projections are reasonable, one should consider whether the implied market share the start-up intends to win over from the local taxi service business is achievable.

The valuation should also account for the start-up’s competitive advantages, if any. A start-up is more likely to maintain high growth rates where it possesses competitive advantages such as a brand name, patent protection or a first mover advantage.[4]

(iii) Estimate terminal value

The DCF method is applied by estimating cash flows for certain discrete periods, followed by estimating a terminal value of the business as of the end of that period. Terminal value accounts for a significant proportion of the overall value of a firm that is a going concern. Accordingly, assumptions underlying terminal value can have a significant impact on the valuation.

The first question to consider is whether the start-up would survive and reach stable growth. While one may be accustomed to reading about the successes of start-ups such as Lazada, Grab and Traveloka in the news, there are many other start-ups that have not or may never make it to stable growth. The probability of failure of a start-up is high and whether a start-up can survive indefinitely must be considered. For example, the Singapore grocery delivery start-up, Honestbee, had successfully raised about $15m in initial funding, but as at May 2019, it had stopped operations of some services in Hong Kong, Indonesia and Thailand.[5] Subsequently, in August 2019, Honestbee filed for a debt moratorium.[6]

If there are factors indicating that the start-up is unlikely to survive indefinitely, for example, if the start-up has a generic business model or an unsustainable competitive advantage, then the value of the start-up is estimated by assuming that cash flows would be generated for a finite period.

If the start-up is likely to survive indefinitely, then the time needed for the start-up would reach stable growth and the estimated long-term growth rate must be considered. It is possible to consider market information such as industry margins to estimate profitability margins of the start-up when it reaches stable growth.

(iv) Estimate capital expenditures and working capital requirements

Start-ups, like any other businesses, will have to reinvest in order to grow. Therefore, in projecting the cash flows, one must consider reinvestments in capital expenditures and working capital. However, start-ups are unlikely to have sufficient internally generated funds to reinvest and they would have to go through several rounds of funding to raise new equity. In such cases, dilution of the existing shareholders’ ownership in the start-up is likely to occur.

Assuming the start-up is generating positive operating earnings, the start-up’s reinvestment rate is calculated by dividing the expected growth in operating income by the return on capital.[7] If the start-up is operating at a loss, reinvestment can be estimated based on growth in revenues and the sales to capital ratio.[8] In order to derive the sales to capital ratio, one can seek guidance from the historical information of the start-up or market information.[9]

It is important to keep in mind that the nature and amount of reinvestments are likely to change as the start-up matures. When the firm has reached stable growth, industry reinvestment rates may also be used to estimate reinvestments.[10]

(v) Estimate discount rate

Discount rate is the rate of return used to convert the future cash flows into present value. A discount rate needs to consider the time value of money, inflation and risk inherent in the ownership of the asset being valued.

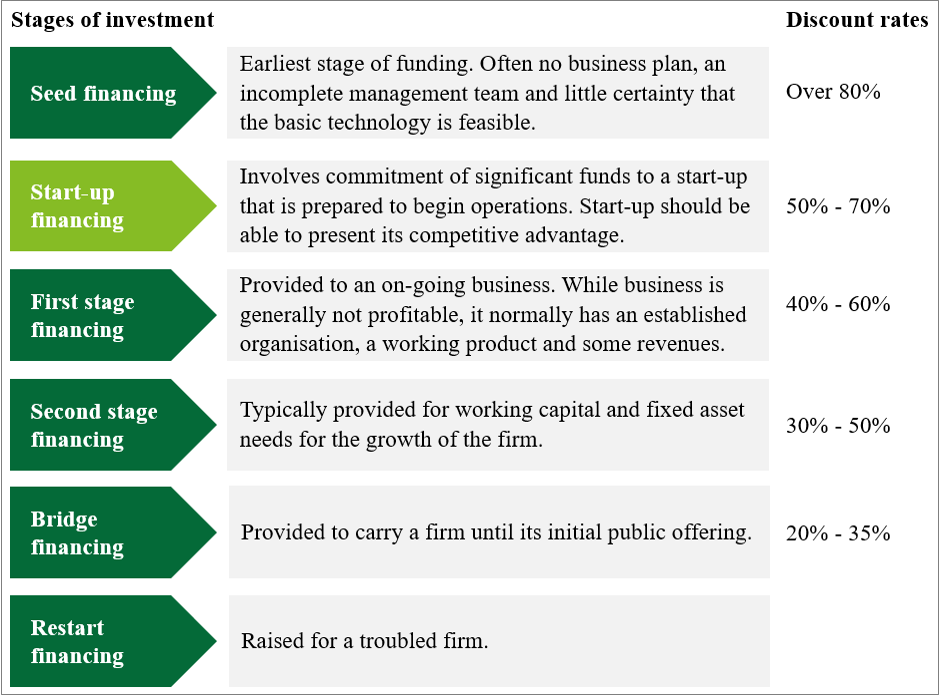

Harvard Business School has considered the discount rates that venture capitalists may apply when valuing high-risk, long-term investments. The stages of investments and associated discount rates are summarised as follows:[11]

It is important to bear in mind that as a start-up matures, the risk profile of the start-up would move towards the industry average and market information can serve as guidance in estimating the discount rate over time. At this stage, the expected cash flows to the firm is discounted at a weighted average cost of capital, which is the cost of the different components of financing used by the firm, weighted by their proportions.

(vi) Estimate value of the firm and equity

The DCF method yields the value of operating assets.In order to derive the value of equity, one must add cash, marketable securities and holdings in other companies to the present value of the free cash flows. It would also be necessary to deduct all non-equity claims on the firm which may be in the form of debts, bonds and preferred equity claims. In cases where the start-up has various classes of preferred and/or common equity, the use of the option pricing model to allocate equity value can be considered.[12]

(b) The market approach

The market approach provides an indication of value by comparing the asset with identical or comparable assets for which price information is available.[13] The market approach is commonly applied in two ways. First, value is derived by considering the prices paid for similar businesses in recent transactions. This is known as the guideline transactions method. Second, value is derived by considering the market multiples of publicly-traded companies. This is known as the guideline publicly-traded company method.

The application of the market approach requires a universe of transactions of businesses and publicly listed companies that are similar to the start-up that one is valuing. From the information gathered on the transactions and publicly listed companies, one must then determine the appropriate multiple to apply in order to estimate the value of the start-up. For example, if a start-up is running losses, applying multiples of revenues may be a better choice compared to multiples of earnings. One could also consider applying units specific to the business being valued,[14] such as number of riders of a ride-hailing service in setting the appropriate multiple. However, before applying such units as multiples, there must be proper consideration of the fundamentals that contribute towards the value of the business, including the robustness of its business model.

When applying the guideline transactions method, it is important to remember that prices from transactions may not be the result of an arm’s length transaction. There may be specific peculiarities to the transaction that had given rise to the transacted price. In this case, it would be useful to collect information on as many transactions as possible and to filter the transactions accordingly. It would also be important to collect information that reflects the value of a business, including growth, cash flows and risk. If a relationship between the transaction value and these variables can be identified, it should be reflected in the valuation.[15]

If resulting from an orderly transaction, the price of a recent investment generally represents fair value and may be an appropriate starting point for estimating the value of the subject start-up. However, when applying this method, the present facts and circumstances must be considered, including changes in the market or in the performance of the start-up.[16]

If there is a probability that the start-up is unlikely to survive indefinitely, one would also have to adjust the value for the probability of failure.

(c) The cost approach

The cost approach provides an indication of value using the economic principle that a buyer will pay no more for an asset than the cost to obtain an asset of equal utility, whether by purchase or by construction, unless undue time, inconvenience, risk or other factors are involved.[17]

It would not be appropriate to value a start-up using the cost approach as the method does not consider the future prospects and earning levels of the business. The cost approach may also not capture all of the intangible assets and goodwill of the start-up.

B. KEY TAKEAWAYS

Valuation is part art and part science. It is not a mere mathematical exercise. It is important for the valuer to have a good appreciation of the business and understand the commercial elements that arise in valuing a business. Amongst others, this includes understanding the business model and competitive advantages of the start-up.

The issues that may arise when valuing start-ups and the valuation framework that can be put in place in order to address some of the issues have been considered. With a proper framework in place, the fundamental elements in carrying out a valuation exercise can be addressed. Consequently, expectation gaps between promoters and financiers can be reduced, and parties can come to a common landing in the fundraising negotiation process.

ENDNOTES:

[1] International Valuation Standards Council, IVS 105: Valuation Approaches and Methods (effective 31 January 2020).

[2] Aswath Damodaran’s website http://pages.stern.nyu.edu/~adamodar/pdfiles/valn2ed/ch23.pdf (accessed 13 September 2019).

[3] Aswath Damodaran’s website http://pages.stern.nyu.edu/~adamodar/pdfiles/valn2ed/ch23.pdf (accessed 13 September 2019).

[4] Aswath Damodaran’s website http://pages.stern.nyu.edu/~adamodar/pdfiles/valn2ed/ch23.pdf (accessed 13 September 2019)..

[5] The Business Times website https://www.businesstimes.com.sg/brunch/show-me-the-money-whats-wrong-with-the-startups-picture (accessed 5 September 2019).

[6] The Straits Times website https://www.straitstimes.com/business/companies-markets/honestbee-given-30-day-extension-of-debt-moratorium-instead-of-requested (accessed 8 January 2020).

[7] Aswath Damodaran’s website http://pages.stern.nyu.edu/~adamodar/pdfiles/valn2ed/ch23.pdf (accessed 13 September 2019).

[8] Aswath Damodaran’s website http://pages.stern.nyu.edu/~adamodar/pdfiles/valn2ed/ch23.pdf (accessed 13 September 2019).

[9] Aswath Damodaran’s website http://pages.stern.nyu.edu/~adamodar/pdfiles/valn2ed/ch23.pdf (accessed 13 September 2019).

[10] Aswath Damodaran’s website http://pages.stern.nyu.edu/~adamodar/pdfiles/valn2ed/ch23.pdf (accessed 13 September 2019).

[11] Sahlman, W.A. (2009). A Method for Valuing High-Risk, Long-Term Investments. Harvard Business School.

[12] Aswath Damodaran’s website http://pages.stern.nyu.edu/~adamodar/pdfiles/valn2ed/ch23.pdf (accessed 13 September 2019).

[13] International Valuation Standards Council, IVS 105: Valuation Approaches and Methods (effective 31 January 2020), para 20.1.

[14] Aswath Damodaran’s website http://people.stern.nyu.edu/adamodar/pdfiles/papers/younggrowth.pdf (accessed 13 September 2019).

[15] Aswath Damodaran’s website http://people.stern.nyu.edu/adamodar/pdfiles/papers/younggrowth.pdf (accessed 13 September 2019).

[16]International Private Equity and Venture Capital Valuation Guidelines (December 2018), para 3.3.

[17] International Valuation Standards Council, IVS 105: Valuation Approaches and Methods (effective 31 January 2020), para 60.1.

AUTHORS

|

Leonard Woo Leonard is a partner within the Valuation & Modelling services team of Deloitte Singapore. He has more than 25 years of advisory experience in business valuation, M&A strategy and transaction advisory. |

|

Chong Su Lyn Su Lyn is an associate director within the Valuation & Modelling services team of Deloitte Southeast Asia. |

Disclaimer: This article is intended for your general information only. It is not intended to be nor should it be regarded as or relied upon as legal advice. You should consult a qualified legal professional before taking any action or omitting to take action in relation to matters discussed herein. This article does not create an attorney-client relationship and is not attorney advertising.

Published 29 May 2020

Follow us on